This new decade, plan your working capital requirements smart. Cash flow for small businesses is the most crucial determinant of whether or not your business will run in the future.

For small businesses, cash is a crucial commodity. The same money is recycled into the business. Over 60-70% of businesses fare on profit, but run low on cash and eventually run out of business. It does not matter if your small business is raking in the profits, readily available liquid cash is of utmost importance. Managing cash can be tricky.

This short guide will help you understand cash flow the way businesses need to – right from how to manage the cash and where to find it if your cash reserves dry out.

What is cash flow for small business?

Cash flow or Working Capital is a financial metric which represents operating liquidity available to a business. Or, to put it simply, cash flow is the money a business uses for its day-to-day operations. It is the amount of money held up in operations.

It is an indicator of the short-term financial position of a business and a measure of its overall efficiency.

The basic formula you need to know to understand cash flow/working capital better:

- Working Capital = Current Assets – Current Liabilities

- Working Capital Ratio = Current Assets / Current Liabilities

Cash flow cycle: A cash flow cycle is the time it takes for a business to convert the net current assets and liabilities to cash.

Important tip from our expert, Mr. Ranganath Iyenger, CA – The longer the cycle, the longer a business is tying up capital in its working capital without earning a return on it.

Positive cash flow:

Your cash flow is positive when the money coming in from sales, accounts receivable is more than the amount you use to pay your vendors, employees and spend money on purchase inventory or raw materials.

Cash inflows exceed cash outflows when a company has a positive cash flow. In other words, a positive cash flow indicates that the business is bringing in more money than it is losing, which is crucial to its long-term success.

Negative cash flow:

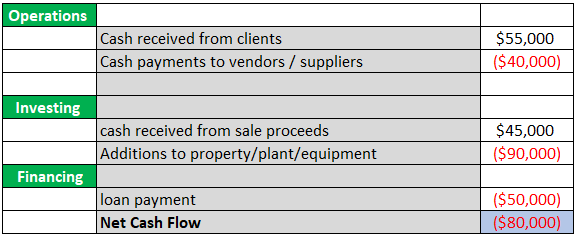

Source: Wallstreetmojo

The exact opposite. A negative cash flow happens when your outflow of cash is more than the cash coming into your business. This does not spell good for a business, but there are steps you can take to fix it.

An organization’s cash flow is negative when it spends more than it brings in. The sales you make cannot cover all your expenses. Financing and investments are the best ways to obtain the necessary funds.

Cash flow positivity vs Profitability

Not many small businesses know this, but there is a lot of difference in being cash flow positive and cash flow profitable. The two concepts are easily misinterpreted and often misused interchangeably.

How to know when your business is cash flow positive: The money coming in and out of your business on any given day is more than the money going out.

How to know your cash flow is profitable: Your income or net revenue is more than your expenses.

What is the difference between Cash Flow Positivity vs Profitability?

A business can be cash-flow positive but may not be profitable. Also, it is possible that a business is profitable but is not cash flow positive.

Keep in Mind:

Cash flow records inflow and outflow of money. For example:

You manufacture your product/service for Rs.500 send out an invoice for Rs. 1000. You are yet to be paid for this.

This entry will be made in your Profit and Loss statement but will not be counted as a cash inflow because you haven’t received the payment yet.

In this scenario – you are still not cash flow positive but you’re profitable by Rs. 500.

Small business cash flow – How much working capital do you need?

According to Strategic interventions Research, Working capital has a direct impact on the cash flow of a business. Small businesses need to know how to balance their working capital – because too much working capital is a bad sign too.

- From a planning perspective, most businesses provide for up to 2 months requirement of working capital and keep about 1 month in contingent reserves.

- Most common sources of working capital (short term) are Equity, Trade Creditors, Factoring, Line of Credit and Short-term loan (< 1 year)

- Laws for MSMEs mandate that they should be paid within 45 days which is the maximum credit extended.

How to fix cash flow problems for small businesses?

Small businesses can maintain cash flow by:

- Determine your breakeven point

- Focus on cash flow management, not just profits

- Maintain up to 1-month cash reserves Use a cash flow worksheet

- Monitor your work in progress, complete and bill timely

- Collect receivables within 45 days

- Encourage customers to pay faster

- Extend payables to the extent possible

- Designate an employee to monitor cash flows

- Liquidate Cash tied up with Assets that are not in use

- Pay suppliers on time to maintain negotiating leverage and terms

- Control expenses carefully especially the small ones

- Watch your inventory and ensure it is neither excess nor short

- Talk to alternative lenders to optimize working capital cost – banks, financial services firms, trade finance firms, factoring firms etc.

- Emergency loans (short term loans) can help to tide over seasonal increases or one-off large orders even if the interest cost is a little high

- Asset-based financing is always useful as it gives you more leeway and if you are using real estate, you can always re-value and increase the collateral once in 3-5 years.

Types of working capital loans for your business:

If all else fails, as it sometimes will, stick to the old fashioned way of getting loans – but be smart about it! Cash flow loans are short term loans, so do not apply for one unless you really need it.

Owner of business:

- Cash infusion as equity

- Fixed Deposits as collateral

Banks & Financial Institutions

- With Collateral – Loan against FDs, Loan against Property

- Without Collateral – Credit Guarantee Fund Trusts (CGTMSE) Collateral free credit Factoring and Bill Discounting

Trade Finance Firms:

- Export Finance

- Supply Chain Finance (PO, Goods in Transit, Inventory, Invoices, Full Supply Chain finance) Merchant Cash Advance

- Online Seller Finance

- Early Payment Funding

- Distributor Receivables Funding

- Just in time Finance

Firms that offer Working Capital Solutions

- Government Institutions – SIDBI, CGTMSE

- Banks/Finance Companies – HDFC, ICICI, SBI, Aditya Birla, Bajajfinserv Fintech Companies – Capital Float, Lending Kart, KredX, Kinara Capital

Bonus: Instamojo analytics will help the small businesses to analyse the number of sales that has happened over a day, a week or a month. In addition to tracking sales, it also identifies your unique customers who bought your products/items.

3 comments

I am so happy I found your blog and I absolutely love your information about manage cash flow small business and the tips you have shared are awesome. I liked and it is wonderful to know about so many things that are useful for all of us! Thanks a lot for this amazing blog!!They offer same information here Gvkfinance.co.nz one must check them also.

Thank you very much for letting us know about how to manage cash flow for small business- tips & guide, it’s difficult for me to get such kind of information most of the time always. I really hope I can work on your tips and it works for me too, I am happy to come across your article.

Amazing info! You can also visit my website bangaloretender for tender information.